Table of Contents

Understanding Your Current Financial Situation

Before embarking on the journey of creating a budget, it is crucial to gain a clear understanding of your current financial situation. This involves a thorough assessment of your income sources and existing expenses. Knowing how much money you earn, and from where, provides a foundation for effective budgeting. Income may come from various channels, including salaries, freelance work, investments, or secondary jobs. Accurately documenting these earnings is the first step in establishing your financial picture.

In addition to income, identifying and analyzing your expenses is equally important. Regular expenditures can be categorized into fixed costs—such as rent, utilities, and loan payments—and variable costs, which may include groceries, entertainment, and discretionary spending. By keeping track of these expenses over a period, you can pinpoint areas where your money is being spent with more clarity.

One useful approach is examining past financial behavior. Review your bank statements and receipts over the last few months to uncover trends in your spending habits. This historical viewpoint allows you to recognize patterns and identify non-essential expenditures, which can significantly aid in crafting a practical budget. Recognizing how lifestyle choices impact your financial landscape may encourage more mindful spending practices in the future.

Moreover, understanding your current financial situation enables you to set realistic and attainable budget goals. Whether you aim to save for emergencies, pay off debt, or make a large purchase, having a complete overview of your financial standing is indispensable. By taking the time to analyze both your income and expenses, you will create a more informed path toward effective budgeting and financial stability.

Gathering Financial Information

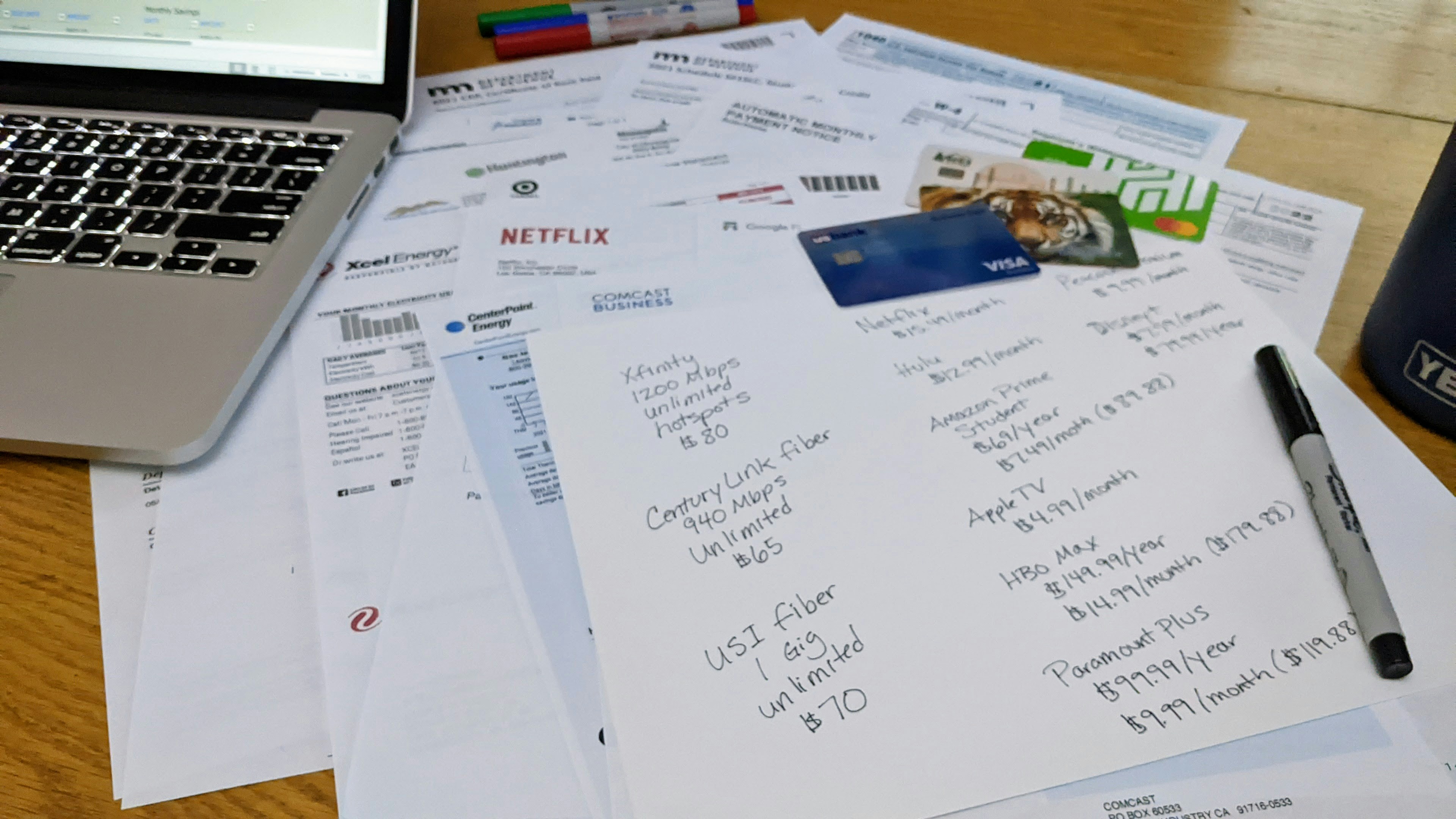

Beginning the journey toward creating a budget requires a thorough understanding of your current financial situation. To gain insights into where your money is going, the first step is to gather financial documents. These documents will serve as a foundational reference that provides a clear picture of your income and expenses.

Start with your bank statements. These statements typically summarize all transactions, including deposits, withdrawals, and any service fees. Aim to collect at least three months’ worth of bank statements to identify spending habits and recurring payments. Next, look for pay stubs that detail your income, including any deductions that impact your take-home pay. Understanding your net income is crucial for effective budgeting.

In addition to bank statements and pay stubs, compile copies of your monthly bills. This includes utilities, rent or mortgage payments, credit card statements, insurance premiums, and any subscription services. Identifying these fixed costs will help you estimate your monthly obligations. Furthermore, consider documenting variable expenses such as groceries, dining out, and entertainment. Tracking these expenditures over a few months can reveal patterns that may otherwise go unnoticed.

To assist in organizing this data, various tools are available. Consider using budgeting apps that sync with your bank account, allowing you to categorize expenses easily. Spreadsheet programs can also be effective for manual data entry and analysis. Select a method that aligns with your comfort level and facilitates easy updates as your financial circumstances evolve.

By gathering and organizing this financial information, you will establish a solid base for crafting a practical budget, enabling you to understand not just where your money goes, but how to manage it effectively moving forward.

Categorizing Your Expenses

Understanding your expenses is a crucial step in creating an effective budget. To begin, it is essential to categorize expenses into three primary types: fixed, variable, and discretionary. Each category plays a significant role in identifying where your money goes, allowing for more informed spending and saving decisions.

Fixed expenses are those that remain consistent from month to month. They are typically contractual and do not change significantly, regardless of your income or consumption levels. Common examples of fixed expenses include rent or mortgage payments, insurance premiums, and loan repayments. Knowing your fixed costs is vital because these are usually unavoidable payments that make up a significant portion of your monthly budget.

Variable expenses, on the other hand, fluctuate each month based on your consumption. These costs include utilities, groceries, and transportation. While they are necessary for daily living, they can vary considerably depending on personal choices and circumstances. By monitoring variable expenses regularly, you can identify trends and make adjustments to reduce unnecessary spending, contributing to a more balanced financial plan.

Finally, we have discretionary expenses, which are non-essential and often tied to personal choices or hobbies. Expenditures in this category include entertainment, dining out, and subscription services. While these costs can enhance your quality of life, they should be carefully managed to ensure they do not undermine your overall financial health. Understanding the difference between discretionary and necessary expenses can help prioritize spending and limit impulsive purchases.

By categorizing your expenses into fixed, variable, and discretionary, you can achieve a clearer picture of your spending habits. This awareness is essential for laying the foundation of a sustainable budget.

Tracking Your Spending

To effectively manage your finances, understanding your spending habits is crucial. This entails regularly monitoring where your money goes, which can be accomplished through various methods. One popular approach is utilizing budgeting apps that not only track expenditures but also categorize them for better analysis. Apps such as Mint and YNAB (You Need A Budget) offer user-friendly interfaces, enabling you to quickly input data and visualize your spending patterns. These tools can provide insights into spending behaviors over time, helping identify trends that require adjustment.

Alternatively, you may prefer more traditional methods like maintaining a spreadsheet. Using spreadsheet software, such as Microsoft Excel or Google Sheets, allows for detailed and customizable tracking. You can create columns for date, amount, category, and payment method, tailoring the layout to suit your specific needs. This manual method offers the benefit of greater control over your data, but it may require more discipline in maintaining updates and accuracy.

For those who appreciate the tactile experience, a budgeting journal serves as another effective tool. By writing down each expense, you cultivate awareness of your spending habits. Not only does this method encourage mindfulness, but it can also be therapeutic, providing satisfaction as you achieve financial clarity. Regardless of the method chosen—be it an app, a spreadsheet, or a journal—consistency is vital. Designate a specific time each day or week to review your transactions, ensuring that you remain engaged with your financial picture. This regular monitoring will empower you to make informed decisions and promote healthier spending habits moving forward.

Identifying Needs vs. Wants

Understanding the difference between needs and wants is fundamental to creating a successful budget and maintaining financial health. Needs are those essential items or services necessary for survival and basic functioning, while wants are non-essential desires that enhance our quality of life but are not strictly necessary.

To effectively identify your needs, you might consider items such as housing, food, clothing, utilities, healthcare, and transportation. These are necessary for basic living and, without them, one cannot sustain a healthy lifestyle. For example, while food is a need, dining out or purchasing gourmet ingredients is classified as a want. Recognizing this distinction helps prioritize expenditures, ensuring that essential needs are met before allocating funds to discretionary spending.

On the flip side, wants can vary greatly depending on individual preferences and lifestyles. Examples may include luxury clothing, the latest electronic gadgets, premium cable subscriptions, or eating at upscale restaurants. While these items can improve your quality of life, they are not vital for daily functioning. To avoid overspending, it is crucial to assess which wants are truly fulfilling and worth the expense.

One effective strategy for distinguishing needs from wants is to implement the “24-hour rule.” This involves waiting 24 hours before making a purchase on anything viewed as a want. During this time, individuals can reflect on whether the item is truly necessary or merely a fleeting desire. Additionally, creating a list of monthly expenses can further clarify where your money goes, aiding in prioritization. By applying these strategies, individuals can make more informed financial decisions that align with their true needs, ultimately fostering better budgeting practices.

Setting Realistic Budget Goals

Establishing a budgeting framework begins with the formulation of clear and achievable goals. When you have little awareness of where your money goes, it is essential to align your budget goals with your current financial status. Begin by analyzing your income sources and fixed expenses, such as rent or mortgage, utilities, and essential bills. Once you have a clear picture of your basic financial obligations, you can identify areas where adjustments may be necessary.

Short-term budgeting goals typically cover a timeframe of a few weeks to months. This may involve identifying specific spending limits for categories such as groceries, entertainment, and transportation. By monitoring these categories closely, you will gain a better understanding of your monthly spending patterns. For instance, if you tend to overspend on dining out, setting a cap on this spending category can help you redirect funds to savings or other essential expenses.

On the other hand, long-term budgeting goals can span several months to years. These often relate to larger financial objectives, such as saving for retirement, funding your children’s education, or preparing for a significant purchase like a home. To establish these goals effectively, consider your life aspirations and the financial stability required to achieve them. A practical approach might include creating a savings plan that sets aside specific amounts regularly, ensuring steady progress towards your long-term financial aspirations.

It is crucial to review your budget goals periodically, as financial circumstances can change. Adjust your goals as needed, taking into account any shifts in your income or unexpected expenses. By setting both short-term and long-term budget goals, you create a dynamic plan tailored to your personal financial objectives, allowing for adaptability while striving for fiscal responsibility.

Creating Your Budget Plan

Establishing a budget plan is a fundamental step towards effective financial management, especially when you are unclear about where your money is spent. The first step in this process is to thoroughly analyze your financial data, which includes income, expenses, and any outstanding debts. Once you have a complete overview, you can start to construct your budget based on your unique financial situation.

There are several budgeting methods available that can cater to different needs and preferences. One popular approach is the envelope system, which allocates cash into different envelopes designated for specific expense categories. This method is particularly effective for controlling discretionary spending, as it physically limits how much you can spend in each category. Alternatively, the 50/30/20 rule is another effective strategy where 50% of your income goes towards necessities, 30% towards discretionary expenses, and 20% towards savings or debt repayment. This rule simplifies the budgeting process and can help ensure that essential financial obligations are prioritized.

When selecting a budgeting method, consider your personal spending habits and financial goals. Some individuals may find the envelope system works best for them as it provides tangible limits, while others could benefit from the flexibility of the 50/30/20 rule. Additionally, using budgeting apps or spreadsheets can greatly enhance the tracking and management of your finances, making it easier to stick to your chosen budget.

It’s also crucial to regularly review and adjust your budget as your financial situation changes. This will allow you to stay aligned with your goals and make informed decisions about your spending and saving practices. By diligently constructing a budget that reflects your needs, you will find greater control over your finances and improve your overall financial health.

Staying on Track with Your Budget

Maintaining adherence to a budget can prove challenging, especially when one is still familiarizing themselves with their financial habits. To successfully stay on track with a budget, individuals must cultivate a systematic approach to managing their finances. A key strategy involves the regular review and adjustment of one’s budget to reflect changes in income or expenses. This flexibility is crucial as unexpected financial situations—such as urgent repairs or medical expenses—may arise.

To begin, setting aside time each week or month to review expenditures can provide valuable insights into spending patterns. During these reviews, individuals should compare their actual spending against the projected budget figures. This practice not only highlights areas of overspending but also offers opportunities for identifying potential savings. Utilizing budgeting tools and apps may aid in simplifying this tracking process, making it easier to maintain control over finances.

Moreover, establishing clear financial goals can motivate individuals to remain committed to their budget. These goals can vary from saving for a vacation to paying off debt. A tangible target often encourages individuals to scrutinize their spending habits and stick to their allocated budget. Additionally, engaging in accountability—whether through sharing budgets with a partner or joining a financial group—can enhance one’s commitment to budgeting.

When the need to adjust a budget arises, it is essential to do so thoughtfully. Modifications should be based on thorough analysis rather than impulsive decisions. Regularly assessing financial priorities can also facilitate informed adjustments. Ultimately, the key to successful budgeting lies in consistent monitoring and a willingness to adapt. By being proactive, individuals can create a sustainable plan that supports their financial stability.

Evaluating and Adjusting Your Budget Regularly

Creating a budget is just the beginning of your financial journey; it is crucial to evaluate and adjust your budget regularly to ensure it aligns with your financial goals and current circumstances. Most individuals find that their expenses and income change over time, necessitating periodic assessments of their financial plans. Regular evaluations allow you to identify areas for improvement and eliminate spending inefficiencies that may have arisen.

Start by reviewing your budget at least every few months, or more frequently if you experience significant life changes, such as a new job, relocation, marriage, or the birth of a child. Make a thorough comparison of your actual spending against your budgeted amounts. This process can reveal surprising insights about where your money actually goes, making it easier to pinpoint categories where adjustments are needed.

Moreover, take the time to celebrate any financial milestones you achieve. Whether it is paying off a credit card, saving up for a vacation, or reaching your emergency savings target, acknowledging these accomplishments not only boosts your morale but also reinforces your commitment to maintaining effective budgeting practices.

When you find areas that need adjustment, be prepared to make those changes in your budget. For example, if you notice consistent overspending in the dining out category, consider reducing that budget by analyzing what you can cut back on. Alternatively, if you have extra income from a side hustle or a raise, you might allocate these funds toward savings or investment opportunities instead. The important thing is to ensure your budget is a living document that reflects your current reality and financial aspirations.

In summary, consistent evaluation and adjustments to your budget not only ensure you maintain financial control but equip you to make informed decisions that align with your evolving financial landscape.